Contributors

Related Articles

To us, the concept of quality is linked to a company’s ability to increase its market share at the expense of competitors, to sell ever more value-adding goods and services, and to expand its leadership in attractive business spaces through innovation and disruption.

During periods of acute market volatility, it is not surprising that investors seek strong assets with defensible businesses or secure long-term values. When markets begin to sell off, investors tend to panic, and we have observed that the number of managers marketing “quality” growth strategies ticks higher.

However, as a long-term investor in innovative growth companies, we know that dealing with volatility is part of our job. We also know that the idea of quality and its integration into an investment strategy is highly subjective and varies by manager and investment process.

For us, the concept of quality is inextricably linked to companies that have the capacity to generate sustainable, above-average growth over time. We believe quality companies are those that can increase their market share at the expense of competitors, sell ever more value-adding goods and services, and expand their leadership in attractive business spaces through innovation and disruption. We believe such businesses are likely to deliver increased cash flows and earnings to their investors and in doing so, are likely to generate above-average investment outcomes. For us, such outcomes are the essence of quality.

Quality Inputs Versus Quality Outcomes

Over the past decade or so, there has been an explosion of methods to quantify investment factors, including quality. Independent quantitative analysts have crunched massive volumes of historical data and conducted extensive back-testing in attempts to break the genetic code of quality. By codifying quality metrics into different measurable outputs, they seek to enable investors to measure and calibrate the quality bias in their portfolios. Index publishers use these measures, which are commonly referred to as factors, to create benchmarks intended to democratize low-cost access to quality. Though the rubrics used to define quality differ somewhat by factor provider, they share a set of metrics that often includes return on equity, financial leverage, stability of earnings and sales growth, net profit margins, and return on invested capital.

As fundamental, business-focused growth investors, we do not initiate our investments based on factor analysis. However, as analysts we are eager to understand any available information that might help our client outcomes. As a result, we regularly review factor attribution and many other common analytical tools. As one might expect, our growth exposure is off the chart, and our value exposure is the inverse. What’s less intuitive however, is that our quality exposure is average to low. MSCI notes that “the quality factor is described in academic literature as capturing companies with durable business models and sustainable competitive advantages.” This sounds awfully similar to our investment criteria, and ultimately, the types of businesses we seek to own.

Select Growth Historical Factor Exposure Ranges

As of 6/30/24

MSCI Factor Classification Standards

The first relates to the criteria used to measure quality. We don’t believe that “stability” in past financial metrics is a sign of quality. Rather, stability could be a sign that a company has not made innovations or changes that alter its short-term operating metrics, or perhaps, that the industry that the company operates in has been relatively static and free from disruption.

The second, and perhaps more important, reason relates to the period of measurement. Any historical analysis will rely on what has happened, over one or many years. However, we believe the objective of investing, particularly growth investing, is to identify what will happen. On this point, our definition of quality diverges quite substantially from the quantitative definition, which focuses on stability and high (past) return on capital.

But before we delve further into our own definition of quality, we should first understand why quality matters. Many academic and industry research studies indicate that “high quality” outperforms “low quality” over long periods. So, given our lower portfolio exposure to quality factors, one might expect our strategies to underperform a factor-neutral benchmark and most certainly a high-quality benchmark or index. However, over our 30 years of investment experience, we have found that is not often the case.

Select Growth vs. Quality Index Win Rate Over Rolling Periods

6/30/01 – 6/30/24

Backward-looking traditional metrics used to assess quality exposure—such as return on invested capital, return on equity, and net profit margin—are not adequate by themselves for assessing future business potential during its early growth stages. This is because they can’t anticipate future gains. In contrast, an active manager can seek to anticipate future gains by using a more comprehensive and qualitative analysis. We believe our value as an active manager comes partly from our ability to analyze unquantifiable qualities in fast-growing businesses.

Seeking Truly Exceptional Businesses

We seek to identify truly exceptional businesses that have the capacity to generate sustainable, above-average earnings growth over time. This is the first pillar of our investment philosophy. We use six investment criteria as a compass to seek to identify businesses whose innovative products and services are disrupting existing markets or creating new ones. These businesses are often differentiated leaders in an attractive business space and boast sustainable competitive advantages. We believe owning companies that can effectively create their own weather can be a durable approach to add value across different markets and economic cycles.

With a global research platform spanning both private and public markets, we strive to identify attractive growth opportunities around the world and at all stages of a company’s lifecycle. Our research analysts are students of secular trends that are driving industry transformations. They have honed their ability to recognize—sometimes before the rest of the market—shared patterns and characteristics of companies that are the major leaders or beneficiaries of these changes.

Our analysts are trying to envision the future. That is a creative exercise that involves anticipating how markets, economies, and society will evolve. Often, the path and duration of major paradigm changes are unknowable, and yet the change itself is inevitable. While we may not know how long that evolution will take, we are highly confident that it will happen. That forward-looking qualitative thought process has helped us build the portfolios we own today.

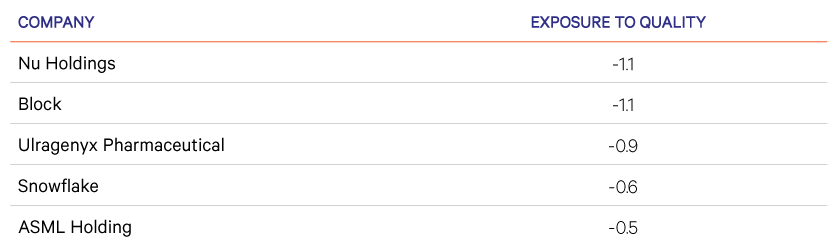

We find many fast-growing businesses across sectors and geographies. Many lie in the intersections of technology and life sciences, commerce, and finance and are disruptive innovators that we expect to have long runways of growth. We believe their visionary services or products and innovative business models position them to generate above-average growth rates in the years ahead. In their early stages, however, these businesses, as shown below, do not always measure well on the basis of backward-looking quality attributes.

Select Growth: Exposure to Quality Factor (Z-score)

Nu Holdings reached 100 million customers in 2024, the first digital bank to do so outside of Asia. It achieved this feat in a little more than a decade, but that growth wasn’t at the expense of profitability: as of 2024’s first quarter, the business generated more than 20 percent return on equity and is the most profitable large consumer bank in Brazil.

Is that not quality?

Block reachieved profitability in 2023 and its adjusted earnings before interest, tax, debt, and amortization (EBITDA) margin hit its all-time high in 2024. Despite strong growth, its Cash App product still addresses less than 20 percent of the U.S. population, resulting in a long growth runway.

Is that not quality?

Ultragenyx is loss-making. However, it’s been granted more FDA approvals than its closest peers in its first 10 years as a public company. It now has five revenue-generating commercial programs and six pipeline programs in late-stage trials.

Is this not quality?

That Which is Essential …

Many of the characteristics that distinguish fast-growing companies are qualitative. Indeed, measuring them can present a challenge to a short-term-focused industry that’s obsessed with numbers and precision. But we believe the characteristics of a business that matter more are those that are uncovered through deep fundamental analysis conducted through a long-term lens and many years of investment experience.

The qualitative nature of evaluating things such as leadership and competitive advantage, in our view, is why they are so often overlooked by traditional measures, or at the very least underappreciated. That is what also creates opportunities for long-term investors. We believe our criteria and investment approach not only steer us toward more sustainable, higher-growth businesses but also toward what, according to our six criteria, we consider to be higher-quality businesses.

Traditional metrics may also be affected by the types of businesses we may invest in. For example, once at scale, network effect businesses have been able to defy the traditional laws of mean reversion for much longer than most anticipate because, by definition, the value of the network grows as each user is added. As a result, the cost of acquiring each additional user declines. This is essentially the inverse of the increasing capital intensity and law of large numbers that typically affect industrial era businesses much more meaningfully. And because these businesses often have poor “quality metrics” during the network effect formation phase, investors focused predominantly on those metrics may miss out on what we believe to be one of the most powerful business models of our time.

The Power of Concentration

Our lower-quality factor exposure (in terms of traditional quality metrics) can be understood by looking at the nature of the companies that we invest in. It also results from our emphasis on constructing a concentrated, conviction-weighted portfolio and our acceptance of short-term volatility in exchange for long-term wealth creation potential, the second and third pillars of our investment philosophy. These aspects of our philosophy are also at odds with quantitative measures of quality.

Exceptional businesses are, by definition, rare. We have found it challenging to find companies that we believe are exceptional and that fit our six criteria. When we find such a business, we want to hold it in a portfolio weight that is large enough to be impactful for our clients. Across our portfolios, we are disciplined to own just 30 to 50 businesses that we believe represent the best growth opportunities within their defined opportunity sets.

Some investors assume that a concentrated portfolio poses a greater risk in terms of higher short-term volatility. Instead, we believe that a portfolio diluted with many holdings may introduce the risk of a permanent loss of capital when the manager doesn’t know the portfolio’s businesses well enough.

Tilting Toward Quality

Obviously, in these trying times, we all want to be surrounded by quality, but quality is in the eye of the beholder. At Sands Capital, for over 30 years, we have consistently used the same six investment criteria to seek to identify the businesses capable of generating sustainable, above-average earnings growth over long periods. We believe that all our portfolios comprise select groups of businesses that, because of their fit with our criteria, are, in our view, of high quality. We believe that by concentrating our investments in these businesses and owning them at large weights for long periods, we will most successfully meet the long-term wealth creation goals of our clients.

Disclosures:

Select Growth v. Russel 1000 Growth Index

Inception date is 2/29/1992. Returns over one year are annualized. The investment results shown are net of advisory fees and expenses and reflect the reinvestment of dividends and any other earnings. The investment results are those of the Select Growth Tax Exempt Institutional Equity Composite. Net returns presented are calculated using actual fees and performance fees if applicable. Past performance is not indicative of future results. GIPS Reports found here.

The companies identified represent a subset of current holdings and were selected by the author on an objective basis to illustrate the views expressed in the commentary. The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients. There is no assurance that any securities discussed will remain in the portfolio or that securities sold have not been repurchased. Individual contributors and detractors are determined using absolute contribution, which multiplies the portfolio weight for each security or group by its total return, calculated and compounded daily unless otherwise stated. The views expressed are the opinion of Sands Capital and are not intended as a forecast, a guarantee of future results, investment recommendations, or an offer to buy or sell any securities. The views expressed were current as of the date indicated and are subject to change. This material may contain forward-looking statements, which are subject to uncertainty and contingencies outside of Sands Capital’s control. Readers should not place undue reliance upon these forward-looking statements. There is no guarantee that Sands Capital will meet its stated goals. Past performance is not indicative of future results. All investments are subject to market risk, including the possible loss of principal. The strategy’s growth investing style may become out of favor, which may result in periods of underperformance. The strategy is concentrated in a limited number of holdings. As a result, poor performance by a single large holding of the strategy would adversely affect its performance more than if the strategy were invested in a larger number of companies. Differences in account size, timing of transactions and market conditions prevailing at the time of investment may lead to different results, and clients may lose money. A company’s fundamentals or earnings growth is no guarantee that its share price will increase. Forward earnings projections are not predictors of stock price or investment performance, and do not represent past performance. Characteristics, sector exposure and holdings information are subject to change, and should not be considered as recommendations. References to companies provided for illustrative purposes only. You should not assume that any investment is or will be profitable. Upon request, a complete list of securities purchased and sold will be provided. To receive a complete list of and description of the calculation methodology for the attribution analysis and complete list detailing each holding’s attribution please contact a member of the Client Relations Team at 703-562-4000.

Notice for non-US investors.